The housing market for landlords is becoming increasingly challenging, as more landlords are selling properties than buying them. A new report from research consultancy BVA-BDRC reveals that, in Q2 2023, over one in ten (12%) of landlords in England and Wales sold properties. In contrast, only 5% purchased properties during this same period.

This trend is being driven by a number of factors, including the rising cost of living, the increase in interest rates, and the uncertainty caused by the war in Ukraine. The rising cost of living is making it more difficult for landlords to cover their costs, while the increase in interest rates is making it more expensive to borrow money. The war in Ukraine is also causing uncertainty in the global economy, which is making landlords less confident about the future. Things that are certain are increased taxation, regulation and rents. Room for more profit then?

The increasing regulation of the private rental sector is a factor that is making it more difficult for landlords. The government has introduced a number of new regulations in recent years, which have increased the costs and responsibilities of landlords. These regulations include the introduction of a minimum energy efficiency standard for rented properties, the ban on letting fees, and the requirement for landlords to carry out safety checks on their properties.

The challenges facing landlords are likely to continue in the coming months. The rising cost of living and the increase in interest rates are expected to continue, and the war in Ukraine is likely to remain a source of uncertainty. As a result, it is likely that more landlords will sell properties or cut back on the number of properties they let.

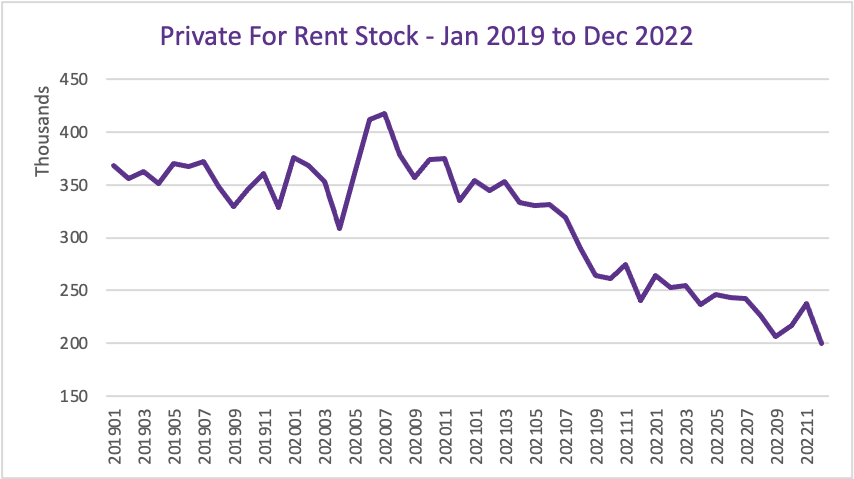

This trend is having a number of implications for the housing market. First, it is leading to a decrease in the supply of rental properties. This is making it more difficult for people to find a rental property, and is pushing up rents. Second, it is leading to a decrease in the number of landlords. This is reducing the competition in the rental market, and is making it easier for landlords to raise rents.

The challenges facing landlords are likely to have a significant impact on the housing market in the coming months. It is important for both landlords and tenants to be aware of these challenges and to plan accordingly.

It is difficult to predict how the housing market for landlords will develop in the coming months. However, it is clear that the challenges facing landlords are likely to continue. Landlords should be prepared for further challenges, including rising costs and increased regulation. Hopefully rents will keep rising to make a fair risk vs reward ratio! If you need help balancing up the numbers on a particular property you are looking at then do get in touch - I can help you crunch the numbers on your next investment for sure!